On SPAR's ($SGRP) Simplification

On SPAR's ($SGRP) Simplification

Sticky, resilient business trading at <3x PF EBITDA with new management following the resolution of a multi-year legal dispute with its founders and divestitures of complex international operations

How often have you been to a grocery or a convenience store and seen unorganized, empty aisles? This is a huge problem for retailers (like Walmart or Dollar General) and product brands themselves (like Coke or Clorox). An unorganized shelf can force customers to buy a different product than usual or, worse, not buy anything at all.

Of course, this may be due to poor demand planning by the retailer or supply issues on the product side. But sometimes, missing products are simply sitting in the back of the store or on aisle floors, waiting to be stocked and organized. In this situation, inefficiency has driven a potential loss in sales and profitability.

Who's in charge of stocking and organizing a retailer? And how can retailers get their stores to look like the below?

Company Overview

SPAR Group ("SPAR", "$SGRP", or "the Company") is a small ($40m market cap) merchandising services company for both retailers and product manufacturers. ~75% of SPAR's revenue comes from its core merchandising and marketing business, in which the Company utilizes its ~25k contractor labor force (provided by independent third parties) to provide services that help maximize product sell-through at retail locations.

One of SPAR's main services is shelf stocking and organization - SPAR touts that it is often physically providing the 'last touch' before products are sold to individuals like us. This involves not only maintaining merchandise levels on shelves but also ensuring that products are well displayed (grouped appropriately with proper labeling, rotated and organized aesthetically, etc.).

The Company also offers a variety of other merchandising services that are important to its customers including display installation, product fixture assembly, and price and inventory audits. The remainder of the Company's revenue comes from store remodeling/renovation services and its growing distribution center business.

SPAR today operates in five countries: The U.S., Canada, Mexico, Japan, and India. Historically, SPAR has leveraged joint ventures with local executive leadership to expand internationally, however the Company is increasingly focused on its core U.S. and Canada businesses, which make up the vast majority of total revenue.

You may not have noticed it, but you've most likely seen a third-party merchandiser at a retailer taking pictures or reorganizing an aisle. This video from CROSSMARK, one of SPAR's competitors, helps provide a good sense of what these merchandisers do in-store:

While some retailers keep merchandising services in-house, there has been an acceleration in outsourcing these functions to third parties like SPAR over time, driven by retail cost control initiatives and difficulty in labor hiring. Advantage Solutions, another SPAR competitor, estimates that the U.S. sales and merchandising services industry is worth ~$8.4bn. I would expect the industry to grow in line to slightly faster than the underlying retail and consumer packaged goods industries (~3% annual growth historically, about in line with nominal GDP growth).

Given the importance of merchandising to retail and brand sales/profitability, the Company has a blue-chip, loyal customer base. 90%+ of the Company's U.S. revenue is from Fortune 500 companies and over 90%+ of the Company's clients have been with the Company for >2yrs. Importantly, merchandising services are provided under 1-3yr contracts that typically have embedded rate increases within them.

While important, it should be fairly clear that merchandising isn't a highly differentiated industry. Different players in the field try to differentiate themselves through technology and incremental services (including marketing), but ultimately merchandisers are essentially outsourced (low-skilled) labor companies.

There are of course switching costs - Merchandisers develop a deep understanding of a retailer or manufacturer's needs and operations after decades-long relationships, especially in particular geographies. That said, one merchandiser could reasonably be substituted for another by a customer in the event of poor service or attempts to increase pricing.

Based on Advantage Solutions' market estimates, the industry is dominated by three players: Advantage Solutions (with ~22% U.S. market share), CROSSMARK, and Acosta (the latter two with ~12-13% U.S. market share each). SPAR is a MUCH smaller player, with an estimated ~1-2% U.S. market share.

This is a key risk for SPAR - The Company is a small, relatively undifferentiated player competing for both labor and customers against companies that likely have more infrastructure, technology, and ability to leverage fixed costs. Larger players also naturally have more negotiating power with customers and a better ability to provide national services.

A Word from our Sponsor: Commoncog

We know the best investors read a lot. But HOW do they learn from what they read? And why do they read so much history? This is a free series of essays that draws from expertise research to explain how you, too, can learn like Charlie Munger.

Situation Overview

SPAR, like the majority of companies I look at, is a company in transition. After years of issues, the Company's new management team is finally simplifying the business.

The largest of these issues was the Company's corporate governance. SPAR is, and historically has been, majority-owned by its founders Robert Brown and William Bartels (we'll refer to them as the "Majority SHs"), owning over 60% of shares outstanding today.

With complete control over SPAR, the Majority SHs unfortunately spent years running the Company solely for their own benefit, disregarding the interests of the other public shareholders. They did this largely through related-party transactions in which the Majority SHs moved money out of the Company (which they ~60% owned) and moved it to other entities (which they ~100% owned).

In just one example, under Majority SH control, SPAR was forced to hire its contracted labor force from an entity owned by the Majority SHs, costing the Company $1m annually that it wouldn't have had to pay otherwise. ~40% of this $1m payment each year rightfully belonged to other public shareholders, but ~100% was essentially transferred to the Majority SHs.

In 2018, after further abuses, SPAR's Board of Directors sued the Majority SHs, leading to a 4yr long legal battle. You can read about the lawsuit in more detail here, including the Majority SHs counter legal actions against the Company.

In 2021, SPAR finally reached an agreement with the Majority SHs. In essence, in return for certain cash/stock payments, assumption of legal costs, and mutual release of all legal claims, the Majority SHs agreed to fully relinquish control over the Company (while maintaining their ownership). Going forward, the Majority SHs cannot control the Board, submit shareholder proposals, or pursue further legal claims against the Company, among other restrictions, hopefully preventing further insider abuses in the future.

During all this disruption, the Company's management team (understandably) completely turned over. Current CEO Mike Matacunas joined in early 2021. Formerly the Chief Administrative Officer at Dollar Tree, Matacunas made several impactful changes early in his CEO tenure for shareholders, including improved segmentation/financial disclosures and restarting quarterly earnings calls (which had been suspended from 2015-2021).

Most importantly, Matacunas quickly announced a full review of strategic alternatives for SPAR (including a potential sale, merger, or go-private). In April 2024, after 18 months, this review culminated in the Company choosing to simplify the business, selling its operations in Australia, China, Brazil, and South Africa, as well as a joint venture in the U.S. The last of these sales should be completed by Q2 FY24.

This is substantial - The portions of the business that are being divested make up 25-30% of FY23 revenue (although a smaller percentage of overall profitability) and have typically exhibited low growth rates given foreign exchange and operating pressures. The Company expects >$22m in gross proceeds from these sales, representing ~50% of the Company's current market cap.

The Company believes these divestitures will help simplify the portfolio, financial structure, and operating model and allow the Company to increasingly focus on its core, growing U.S. and Canada businesses.

To summarize, FY24 will be the first year for the Company under new management/control without issues related to the Majority SHs, legal costs associated with the strategic review, and headwinds related to the Company's international operations.

Analysis

There are quite a few aspects of SPAR's business that aren't particularly great.

Given the competitive nature of the industry and SPAR's position as a smaller player, I would expect the Company's revenue growth to be somewhat constrained. The Company's U.S. merchandising division did grow 20% YoY in FY23, however price vs. volume was not broken out - I get the sense that a substantial portion of this increase was simply due to inflation passthrough and one-time renegotiation of major contracts (which hadn't been updated for years before the new management team's arrival).

That said, I don't think it's unreasonable to believe the Company can grow in line with the overall industry (low-single-digits) given sticky customer relationships, opportunities for further outsourcing penetration, and above-market growth from remodeling/renovation and distribution center services and increasing penetration in Canada. For context, the Company's overall U.S. revenue has grown at ~3.5% annually since FY19.

The company also suffers from a customer base made up of large, highly cost-conscious retailers and manufacturers with strong negotiating power. Not only does this limit the Company's ability to grow revenue and margins, but it importantly impacts the Company's ability to generate cashflow, given customers like Walmart and Clorox can exert difficult terms on SPAR.

In FY23, the Company's customers on average paid SPAR's invoices in ~90 days, whereas the Company on average paid its contract labor force in less than ~30 days. This means that SPAR's business model constantly consumes cash as it grows (contract labor is paid months before the Company is paid by its customers).

Given these cash considerations, SPAR seemingly has to draw on its revolver to finance day-to-day operations. While the Company's business is stable and seemingly resilient enough to lend against, there are always potential risks when utilizing debt, particularly if we see a macro slowdown.

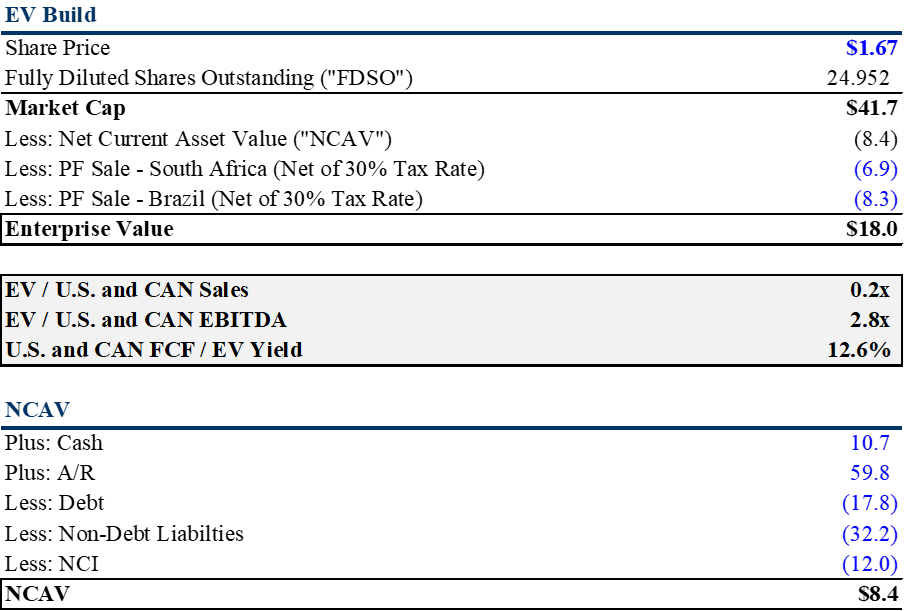

All that said, SPAR is trading cheap when giving the Company credit for its recent divestitures and large outstanding receivables balance. My calculation of the Company's enterprise value and valuation multiples are below (based on estimated PF financials for the core U.S. and Canada businesses):

At <3x PF EBITDA and a ~13% PF FCF yield, the market seems to be implying 0% revenue growth for SPAR going forward. This seems too low to me, particularly given the Company's sticky customer base and the aforementioned potential growth drivers.

While the Company's capital allocation going forward is still relatively unclear, management has hinted at proceeds from the recent divestitures being used for M&A and potentially shareholder distributions (dividends/buybacks). For what it's worth, CEO Matacunas got seemingly attractive deals on the recent divestitures, helped integrate Family Dollar into Dollar Tree in 2015, and even was CEO of a PE firm called Five Hill Capital for 3yrs prior to becoming CEO of SPAR. We'll see if that translates into value-accretive capital allocation going forward.

With minimal organic growth opportunities within the industry, I think SPAR could be an acquisition target in the future for one of its larger competitors. The Majority SHs are now close to their 80s, and with little to no influence over the Company, they may be interested in selling at some point soon.