On Beenos ($TSE.3328) and Buyee

Despite rapid, profitable growth at Buyee, an innovative internal culture, and recent share repurchases, Beenos trades below the value of its venture portfolio and net cash

Company Overview

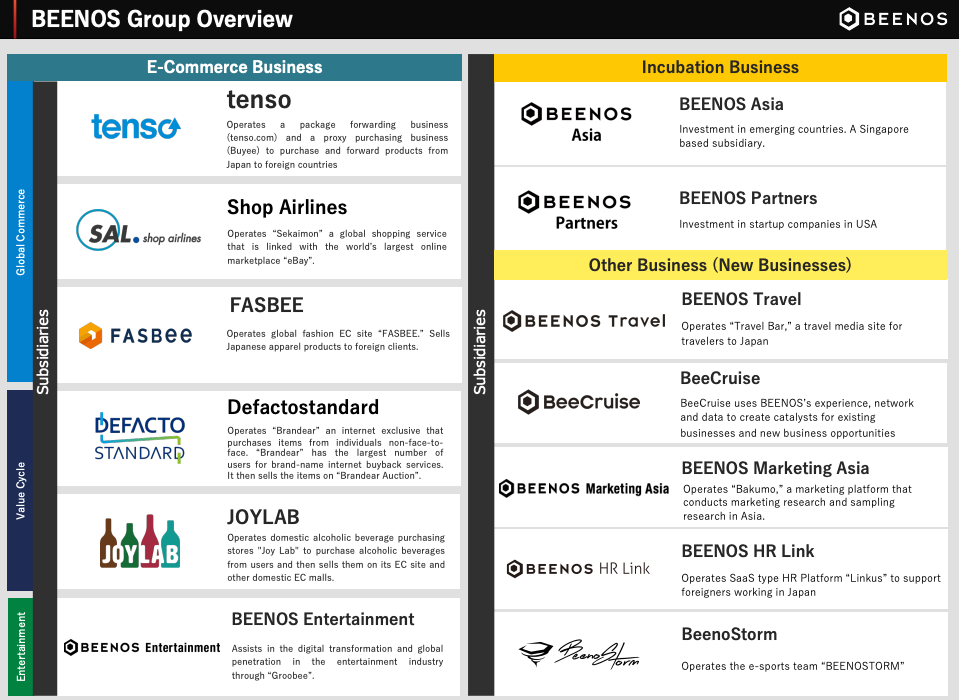

Beenos ("$TSE.3328" or "the Company") is a ~¥26bn / ~$170m Japanese microcap that owns and operates e-commerce and other technology platforms both domestically and abroad. With multiple underlying segments, businesses, and global investments, Beenos can be quite a difficult business to navigate from the outside (despite English financial reporting).

To keep things as simple as possible, we'll focus only on the two core drivers of Beenos' business value. The first is the Company's Global Commerce segment, which operates websites that help customers abroad purchase items directly from Japan, providing translation, currency exchange, and shipping services.

The Company's main asset in Global Commerce is Buyee, Japan's largest proxy purchasing service. 'Proxy purchasing' simply refers to a service where a third party places and handles orders on a customer's behalf.

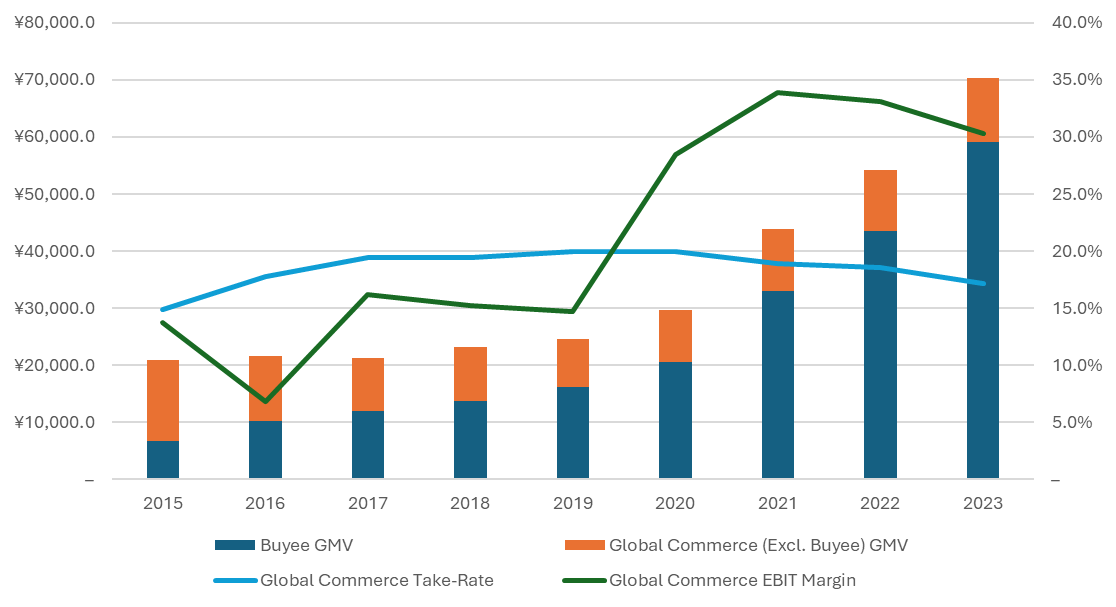

Today, Buyee accounts for ~¥60bn / ~$400m of gross merchandise value ("GMV", i.e. the total value of goods purchased on the platform) annually, selling everything from Japanese skincare products to Nintendo Switches to high-end Seiko watches from partner websites like Yahoo! Japan, Mercari, Rakuten, and thousands of others. Importantly, customers place orders in English (or a variety of other languages) directly on the Buyee website, without having to navigate to any partner websites (that are typically in Japanese).

We'll discuss Buyee more shortly, but the platform's growth has been pretty incredible. Buyee was started internally in 2012 to disrupt its predecessor, tenso.com, one of the Company's other Global Commerce platforms. While tenso.com accounted for ~60% of segment GMV in FY15, this fell to ~10% by FY23, driven by rapid Buyee growth (now ~85% of GMV).

Buyee has grown its GMV at a ~30% CAGR since FY15 and currently has an estimated EBIT margin of ~30%. Global Commerce as a whole is expected to produce ~¥4.2bn / ~$27m in operating profits this year with minimal working capital (no inventory requirements).

Results have been particularly strong post-COVID, with increasing global interest in Japanese culture. More recent results have been positively impacted by the depreciation of the yen, which is currently the lowest in the last ~35yrs, and aggressive marketing campaigns (including discount coupons for products and international shipping fees), driving a declining take-rate (revenue / GMV) in FY23.

Disruption of the Company's own products is deeply embedded in Beenos' culture. The following excerpts from recent Beenos Q&A sessions describe this dynamic well:

"People often assume that our biggest strength is in Global Commerce when, in fact, our biggest strength lies in the ability to create new businesses. We believe that it is important to develop these businesses to where they become able to generate profits and show consistent growth." - Q4 FY21 Q&A

"I see the primary challenge as the heavy reliance on Global Commerce. Consequently, our focus is on diversifying our business portfolio to establish a company with multiple pillars. To achieve this goal, we are actively developing new ventures and forging partnerships with our investees to launch new businesses." - Q1 FY24 Q&A

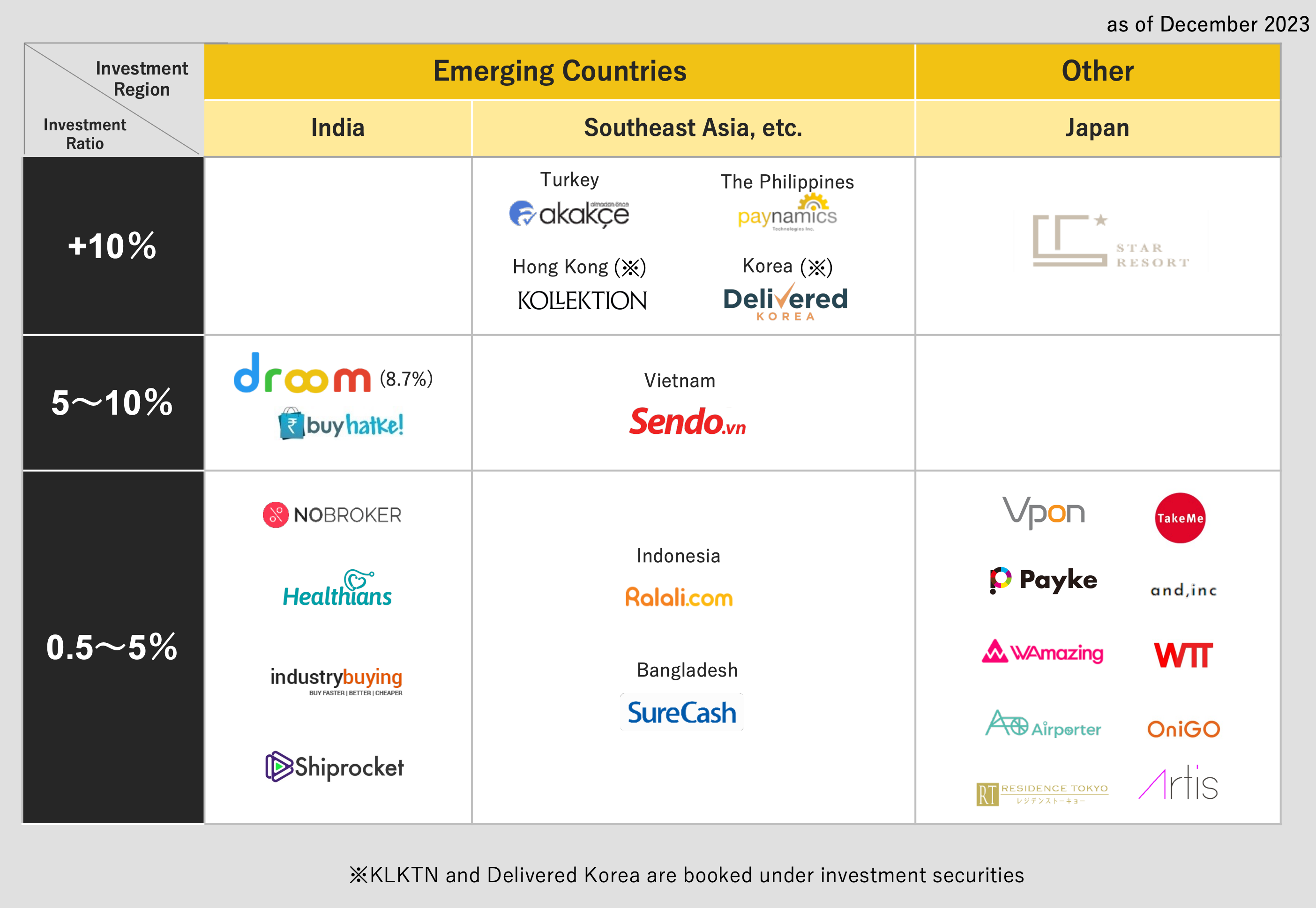

That takes us to the Company's second, and arguably more important, segment: Incubation and Other Businesses. Value in this segment is mostly from the Company's venture portfolio (called "Operational Investment Securities" on the Company's balance sheet), which invests in e-commerce and other online platforms, with a focus on online marketplaces and payments in emerging markets in Asia (excluding China).

This portfolio has 15 investments in Japan and 43 overseas. Major investments can be seen below. A notable previous investment in this portfolio was the Indonesian super-app GoTo, which the Company exited recently in Q4 FY23 for ~¥2.5bn / ~$16m.

The book value of the Company's Operational Investment Securities on the balance sheet was ¥3.9bn / $25m at 9/30/23, but management believes the market value of the portfolio is closer to ¥21.7bn / $142m. These are private investments that are difficult to independently value, so there's a risk that management is being too optimistic. Regardless, it's clear the Operational Investment Securities are material relative to the Company's entire market cap.

This segment also includes the Company's internal efforts to build new businesses, which are often growing but money-losing. Notable new businesses include a cross-border support business (which is actively trying to disrupt Buyee), an inbound tourism business, and a cross-border HR business.

I won't get into these businesses in more detail, but Beenos' entrepreneurial culture is important. It's like the quote often attributed to Charles Darwin: "It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most adaptable to change."

The same is true for businesses. Beenos is its own biggest competitor and is constantly on the lookout for new opportunities that can grow like Buyee has, improving the Company's chances of long-term survival. Jacob McDonough dove into Beenos' ability to 'spawn' new businesses here.

Importantly, Incubation and Other Businesses are largely self-funded, in the sense that the Company's policy is to sell Operational Investment Securities to offset upfront costs for new businesses and corporate costs. However, given the venture portfolio is largely private, the timing of sales may be difficult to predict.

Astute readers by now will have picked up on Beenos' valuation. At the current price, you can buy Beenos at a ~¥26bn / ~$170m valuation. That's for a business that does ~¥4.2bn / ~$27m in operating profits growing revenue 30% annually through Buyee and owns a venture portfolio that is worth ¥21.7bn / $142m. That excludes ¥6.7bn / ~$44m in net cash on the balance sheet (inclusive of the Company's recent sale of its Defactostandard and JOYLAB businesses).

Said differently, the Company's venture portfolio and net cash are greater than the current market capitalization of the Company. If you had $170m in cash, you could buy all of Beenos' shares, sell the entire venture portfolio at management's estimated market value and pocket the net cash on the balance sheet, making back all of your money and then some, while still owning Buyee, a rapidly growing and profitable business.

That's not realistic and is far too simplistic, but it gives you a sense of the valuation discrepancy here. Is that valuation fair? Given unknowables related to the venture portfolio, it largely comes down to what you think Buyee is worth today.

Buyee Overview

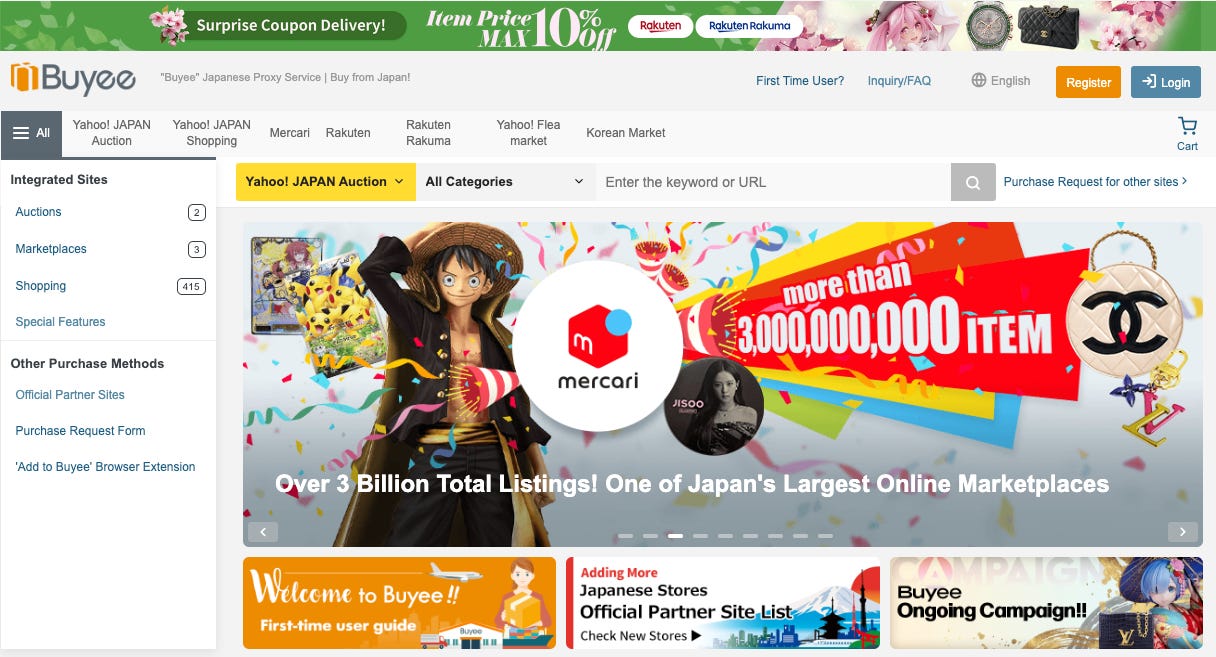

On Buyee, a customer can purchase from ~5k Japanese companies (referred to as Buyee "partners") without going directly to Japanese e-commerce websites. Instead, Buyee works with its partners to host translated product information directly on the Buyee website, allowing customers to shop confidently and in the language of their choice.

When a purchase is made, Buyee places the order with the partner on the customer's behalf. Goods are received at Buyee's warehouse in Japan (and can be held there for up to 30 days), and are subsequently shipped to the customer abroad. If multiple items are purchased from various stores, Buyee offers a bundling (i.e. consolidation) service.

Buyee charges ¥300 / $2 per order that it receives as revenue, however customers are separately charged for shipping fees based on weight and can pay additional fees for services such as insurance, photo service, etc. Importantly, partners are not charged for Buyee's services.

If you're wondering who's buying items off of Buyee, it's largely enthusiasts interested in niche (non-essential) products. The top product categories are figurines, games, car and motorcycle parts, luxury fashion, and CDs, with most items being pre-owned. The top 5 countries in terms of sales are the U.S., Taiwan, Hong Kong, Singapore, and the UK.

A whopping ~25% of goods purchased on Buyee are anime-related. This is a growing industry - Per the Association of Japanese Animations, the Japanese animation industry was worth ~¥2.9tn / ~$19bn in 2022, doubling over the last 10yrs. Importantly and surprisingly, ~50% of all revenue in the industry now comes from outside Japan.

Customers usually aren't buying from Buyee (or Japan in general) for cheaper goods. Instead, this is really a service for die-hard customers to buy unique Japanese items that can't be found locally. Given this, Buyee's customer base is more recurring than you would expect. ~90% of purchases in Q1 FY24 were made by existing customers.

You'll note that this is not a particularly differentiated offering. Buyee operates in a highly competitive industry against players like Zenmarket, Neokyo, and From Japan. Barriers to entry are low - Any individual can set up shop and become a proxy for Japanese goods if they can speak or translate Japanese and have access to Japanese stores. Buyee's partners are also not exclusive - They can, and do, work with multiple proxy services.

Given these dynamics, customers seem to choose which proxy service to use based on which is the cheapest and, to some extent, which has the best service. This is a helpful Google Sheet that compares the costs of various proxy services in Japan. Buyee is one of the cheaper services (although it charges additional for add-ons), and seems to have more extensive promotional campaigns than its competitors.

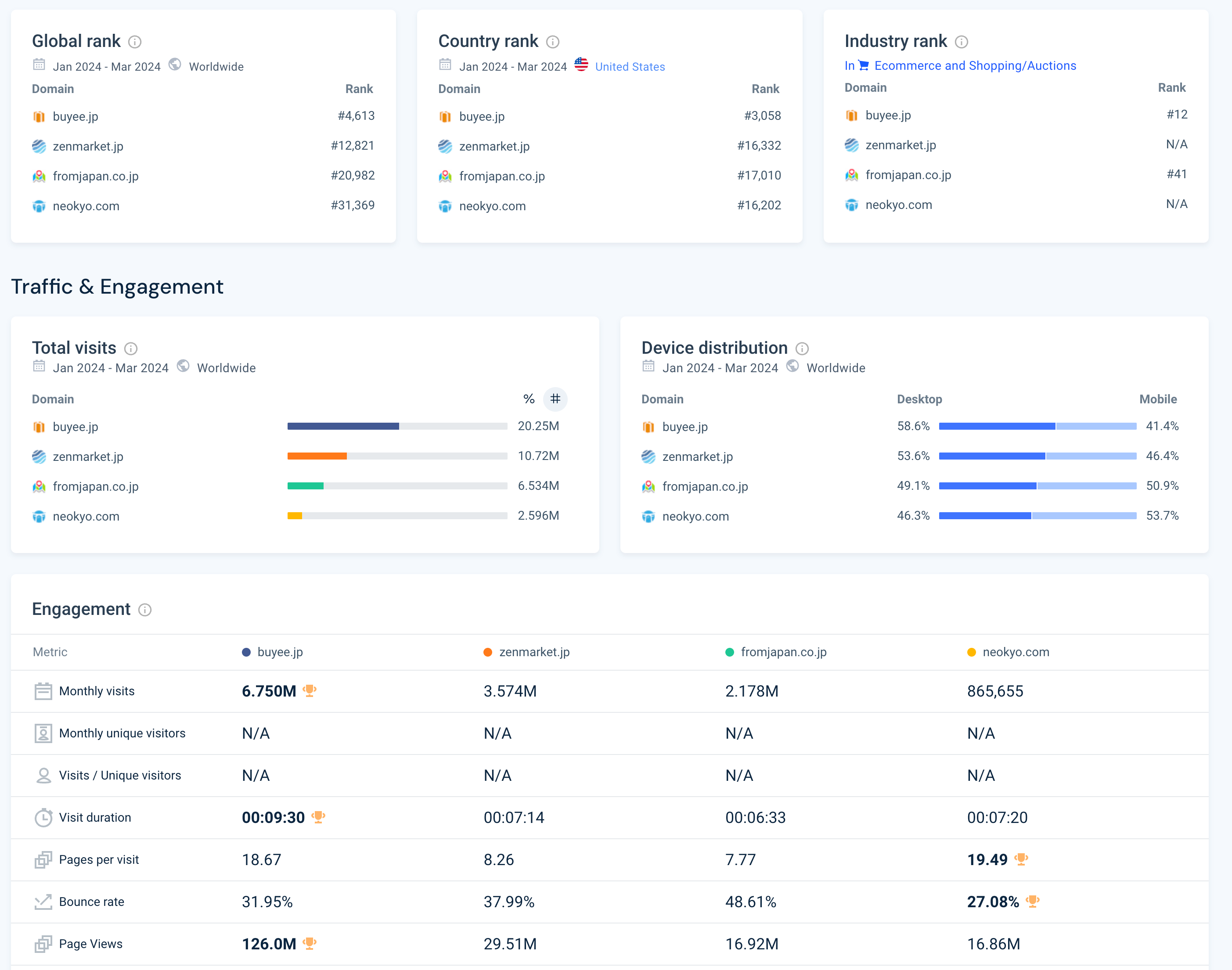

That's not great, given that's essentially a race to the bottom. There's always a risk that a competitor impacts the economics of the industry by suddenly spending unprecedented amounts on promotions. However, at the moment, Buyee is best positioned given it's the largest purchasing service in the country, leveraging its scale to pass savings on to customers. You can directionally see the Company's website traffic relative to competitors below (per Similarweb).

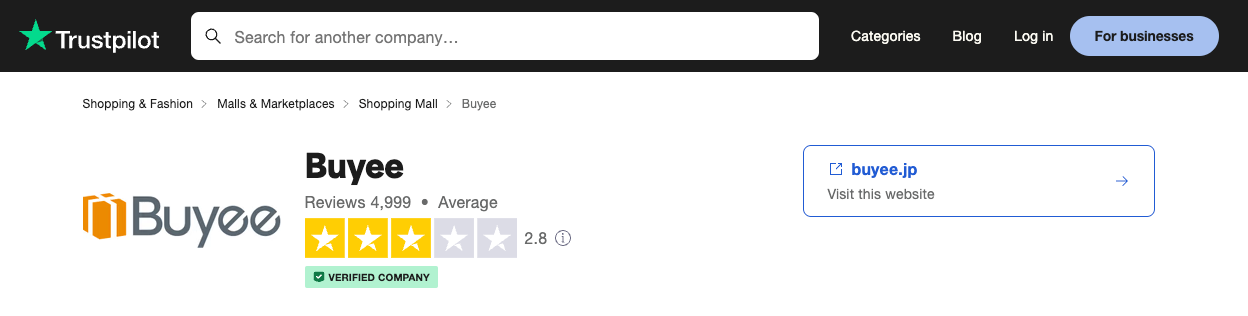

However, this doesn't tell you the full story. One look at the Company's reviews online shows you that customers aren't happy. This may be a vocal minority, but certain feedback is common - Buyee has poor customer service, occasionally loses packages, and tends to have a higher all-in cost after accounting for shipping and FX fees.

This is a key risk - With minimal differentiation between competitors, customers can easily switch to other proxy services after a negative experience. Buyee has a scale advantage that it doesn't seem to be effectively using with regard to costs and service.

Certain changes are being made over time - For example, Buyee reduced fees across the board in late 2022 and waived consolidation fees. Last year, Buyee started to dispose of unnecessary original boxes when consolidating orders, reducing weight and thus shipping costs for customers. Hopefully this continues.

I think Buyee does have a separate (and possibly more sustainable) competitive advantage that's driving revenue growth - Distribution. As a Japanese company itself (unlike key competitor Zenmarket), Buyee has longstanding, close relationships with Japanese partner businesses, notably Mercari (the most popular community marketplace in Japan) and Yahoo!. I estimate these partners make up a substantial portion of the Company's total revenue.

Buyee is the official proxy partner for both Mercari and Yahoo!, being featured prominently on partner websites when customers are shopping and trying to ship abroad (see below). This makes sense - These partners presumably don't want to build out their own cross-border logistics and shipping infrastructure when Buyee is providing them this service for free.

Of course, there's a risk these partners could go directly to customers (which Rakuten seems to be trying). However, that seems like a tough decision to make when Buyee is offering its service at no cost. This is reflected in partner retention - Churn is <1%. We'll see, but this is another risk to monitor.

Analysis

What's a business in a growing industry with a scale and distribution advantage, minimal working capital and capex requirements, and >30% operating margins from a recurring customer base worth?

Despite being a tech company, this is not a B2B SaaS business and shouldn't be valued like one. You could compare a platform like this to other consumer platforms like eBay or other Japanese cross-border players like Raccoon Holdings (which I have not studied).

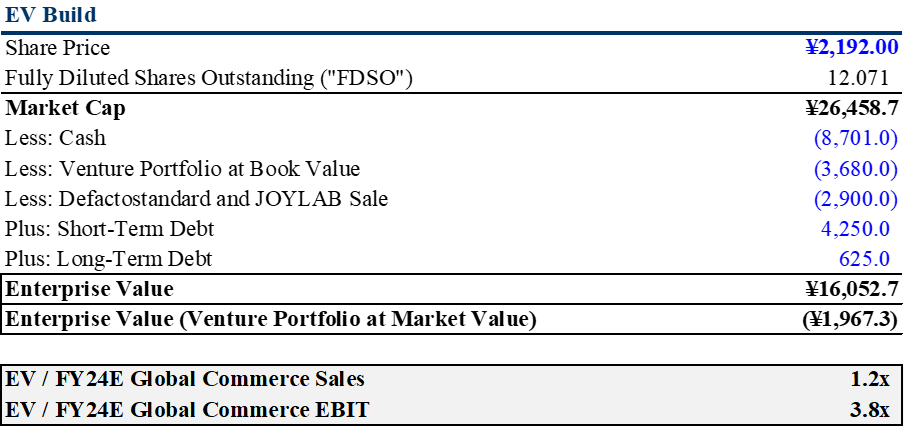

The analysis here should be much more simplistic than that. I don't know the exact multiple Beenos should trade at, but I do know a business like Buyee shouldn't be trading for free in the marketplace (regardless of a 'Japan discount'). My calculation of the Company's enterprise value and valuation multiples are below:

If the venture portfolio is worth what management says it is, then Beenos is trading below its liquidation value (i.e. the Company is worth more dead, with all its assets sold, than alive). If we assume the venture portfolio is worth just book value (which is conservative), then an incoming investor is essentially buying Buyee at <4x EBIT.

We've discussed some of the risks associated with Buyee, all of which are real. Still, that valuation essentially implies no growth going forward. That doesn't seem realistic to me given growing global interest in Japan/anime, Buyee's scale and distribution advantages, and the Company's track record over the last 10yrs.

The valuation simply seems too low for a business with Buyee's characteristics, especially considering we're not giving the Company any credit for its growing Entertainment segment or its smaller new businesses.

The market could be concerned that the venture portfolio value will never be realized, but that's not in line with what the Company is communicating. There have been multiple indications from the Company that the venture portfolio will be sold down over time (see below), but of course, the timing will be unpredictable.

"We are also in our monetization phase of investment securities in the Incubation Business. However, it is not in our interest to maintain this pace in investing/accruing losses but to develop businesses that are profitable. Our mission is to create more businesses like Groobee that will spin out of the Other Businesses segment into the E-Commerce segment and increase its GMV to the point where they become profitable." - Q2 FY23 Q&A

That brings up another risk - Investors may have a view that Beenos is burning all its cash and proceeds from its venture portfolio on money-losing new businesses. This is a valid concern - The exact return the Company is getting on its reinvested capital is difficult to pinpoint. That said, the Company has a track record of standing up new businesses, most notably Buyee itself which has obviously been extremely successful.

Could that happen again? Who knows. But more importantly, not all capital is reinvested into Incubation and Other Businesses (which are largely self-funded through sales of Operational Investment Securities). The remaining capital is returned to shareholders through dividends and buybacks.

Buyee currently has a ~1% dividend yield and bought back ~4% of shares in FY22 and ~2% of shares in FY23. At the current valuation, I'd like to see further share repurchases, but I appreciate the Company's commitment to disrupting itself. We'll likely see continued repurchases along with reinvestments into new businesses, which I think more than justifies a higher valuation.