On EML Payments ($ASX.EML) Returning to its Roots

After cutting problem assets and implementing new management, EML trades at ~5x EBITDA despite historically sticky revenues, double-digit growth, and consistent profitability

Situation Overview

EML Payments ("EML", "$ASX.EML", or "the Company") is a small (~AU$260m market cap) Australian payments company, with a focus on prepaid card solutions globally. Today, the Company operates in 27 countries and has ~1,000 customers.

Unlike debit/credit cards, 'prepaid' cards are loaded with money in advance and do not pull funds from a bank account. Cards can either be non-reloadable (i.e. one-time use such as gift cards) or reloadable. They can also either be physical or digital.

At a high level, EML typically acts as program manager and processor for customers (corporations, governments, etc.) wanting to offer prepaid cards to their end-users. This involves things like physical card issuance and activation, relationships with vendors, fraud and risk management, customer support, authorization (i.e. approval/denial of transactions), and ultimately clearing and settlement.

In most regions, the Company is licensed to self-issue its prepaid cards, and in these cases, holds prepaid customer funds on its own balance sheet (earning interest on these balances). In the U.S., where only banks with FDIC insurance can hold customer funds, EML partners with banking 'sponsors'. Importantly, the Company does not take on credit risk - Again, these cards are all pre-funded, with no credit being extended by the Company.

Prepaid card use cases vary widely across the industry, and EML is highly diversified across applications. The Company is a leader in the mall gift card market in North America and Europe and salary packaging in Australia (a tax incentive that allows for payment of certain expenses with pre-tax income), with other key verticals including corporate incentives, government welfare payments, and gambling payouts.

EML is a high-quality, attractive business - Revenues are diversified across customers and end-markets, customer contracts are sticky (often multi-year and exclusive, with substantial switching costs), and sales are re-occurring (albeit not truly 'recurring' - Revenue is heavily impacted by purchasing volume).

EML also plays in a rapidly growing market with expanding use cases, driving strong historical revenue expansion well into the double digits. EML indicated that its payments-related volume (referred to as gross debit volume ("GDV")) from existing customers grew ~30% YoY in FY19 (FYE 6/30). The Company has estimated 15%+ annual growth rates for underlying prepaid card markets through 2030.

Importantly, the Company generates strong profitability (~75% gross margins, ~25% EBITDA margins) with real FCF conversion (I would estimate ~50% on a normalized basis). This is further magnified by significant operating leverage inherent in the business model (minimal incremental overhead to support additional purchasing volumes), helping drive an incredible ~82% EBITDA CAGR from FY15-FY19, of which ~68% was organic.

Despite these fundamentals, EML has struggled greatly over the past 5yrs, with the Company's stock falling a whopping ~90% since its 2021 highs. Why?

EML's post-COVID journey has been long and complex. I'll discuss at a high level below, but there's much to the story I won't cover in the interest of time. I point you to Jeremy Raper's detailed pitch on the name here, particularly the extensive 'Business Background' section for more.

Following a period of rapid, very successful growth (organic and inorganic) from FY12-FY19 that saw the Company transform from an Australian-focused prepaid cards business with <AU$4m in revenue to a global business with thousands of prepaid card programs, the Company made two ill-fated acquisitions in Europe: Prepaid Financial Services ("PFS"; Acquired in April 2020 for ~AU$250m) and Sentenial (acquired in September 2021 for ~AU$115m).

Not only were the acquisitions material and expensive, but they also diversified the portfolio from the Company's core strengths into new verticals such as banking-as-a-service and open banking. In addition, these acquisitions were poorly diligenced (potentially improper conduct/fraud incidents later discovered at both companies) and proved difficult to integrate (operational complexity, regulatory issues in new geographies during COVID, etc.).

Most damaging were issues with PFS post-acquisition - In 2021, regulators raised "significant regulatory concerns" with regards to PFS (risk and controls, anti-money laundering process, governance, etc.) that necessitated substantial compliance-related investments to rectify. PFS growth was ultimately capped by regulators until underlying concerns were resolved (they never would be). This, along with incremental investments, drove substantial margin declines for the Company.

A class action lawsuit was filed by shareholders around this time. The coming years saw materially declining sentiment and numerous corporate changes, including an overhaul of C-suite and board-level personnel, activist involvement, and ultimately a formal strategic process to sell parts or all of the Company. For what it's worth, the Company publicly confirmed takeover interest in 2022 from Bain Capital and two other parties. While discussions ultimately ceased, this is a strong indication of the value in the Company's core operations.

The strategic process culminated in the January 2024 decision to liquidate ~60% of PFS by early 2025 (100% loss on this portion of the business, known as PCSIL; the UK portion of PFS, known as PFSL, is growing/profitable, has no remaining regulatory issues, and remains with the Company) and the March 2024 announcement to sell Sentenial for ~AU$54.1m (~50% loss) to GoCardless (completed in September 2024).

The market reacted positively to the Company's actions to jettison its problem acquisitions, with EML's stock trading as high as ~AU$1.27 in March 2024. Unfortunately, the reaction was short-lived, exacerbated by selling pressure from major shareholders Alta Fox (activist; Given achievement of their goals) and First Sentier (fund termination/liquidation), representing ~20% of shares.

So where are we today? After years of missteps, regulatory issues, and poor trading performance, market sentiment towards EML is (understandably) completely bombed out.

But looking at the situation from an outside perspective, EML today looks a lot like it did in FY19, when the Company was growing at rapid rates and consistently generating cash, only with the addition of the growing, profitable PFSL business and a higher interest rate environment driving incremental 100% margin cashflows.

Legacy issues with PFS and Sentenial are largely behind the Company, with minimal remaining liabilities. Proceeds from the Sentenial sale will help transform the balance sheet and drive a close to net cash position. Importantly, this will allow the entire organization to return focus to core operations (which have shown some deterioration over the past few years).

This is a key focus for the new management team and board (including CEO Ron Hynes, who joined on 6/30/24 and has an extensive background in prepaid cards), who are doubling down on organic growth through expected investments in go-to-market and technology (to be communicated to the market in more detail at the 11/26/24 AGM). The team has also shown strong operating discipline, successfully slashing costs to date to drive efficiencies.

Despite the positive momentum, the Company trades very cheaply today, >10% below levels prior to the announcement of the PCSIL liquidation and ~50% below levels after the announcement of the Sentenial sale.

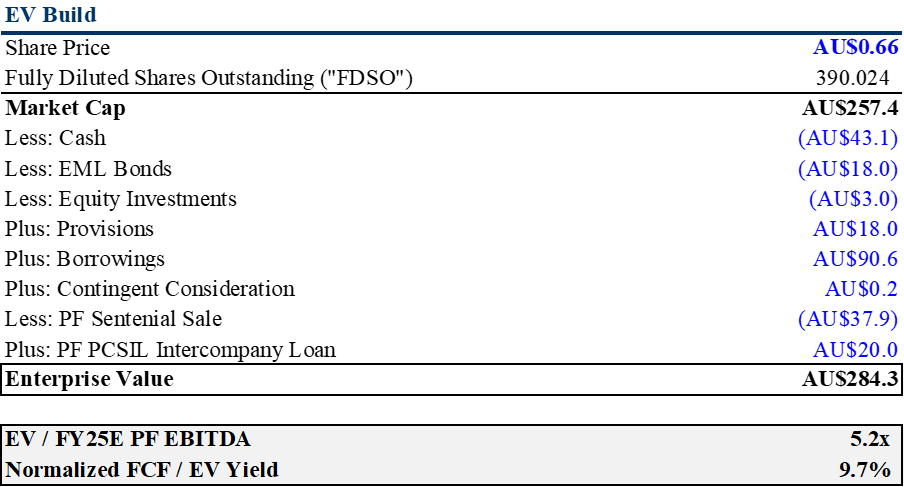

My calculation of the Company's enterprise value can be seen below:

Notes:

EBITDA is adjusted for IFRS-16 (lease payments are deducted from operating profits).

FY25E EBITDA based on management guidance, adjusted for leases. Appears achievable given historical profitability of the Company

Normalized FCF based on 50% FCF to EBITDA conversion, in line with historical levels and management's medium-term operating cash flow conversion target

'PF Sentenial Sale' proceeds arbitrarily adjusted for taxes (~30% assumed)

'PF PCSIL Intercompany Loan' refers to remaining PCSIL exposure (i.e. cash burn incurred and expected, including payment of one-time expenses). Payment expected to be made in early 2025

I estimate the Company trades at ~5x FY25E EBITDA and a ~10% normalized FCF yield. The Company is not out of the woods yet - New management will need to demonstrate a return to consistent growth and profitability, but current multiples seem too low for a company of this quality and historical growth profile, particularly given prior acquisition interest from third parties.

The upcoming AGM, which will provide management's medium-term strategies and growth outlook, could prove to be a catalyst for a re-rating.

The rest of this article will cover EML's business model and operations in more detail.

Company Overview

EML can be hard to get a handle on given its highly diversified operations (different underlying growth rates, margins, etc.), disclosures (multiple ways to cut up the business), and a range of corporate changes (acquisitions and subsequent divestitures) over the past few years muddying financials.

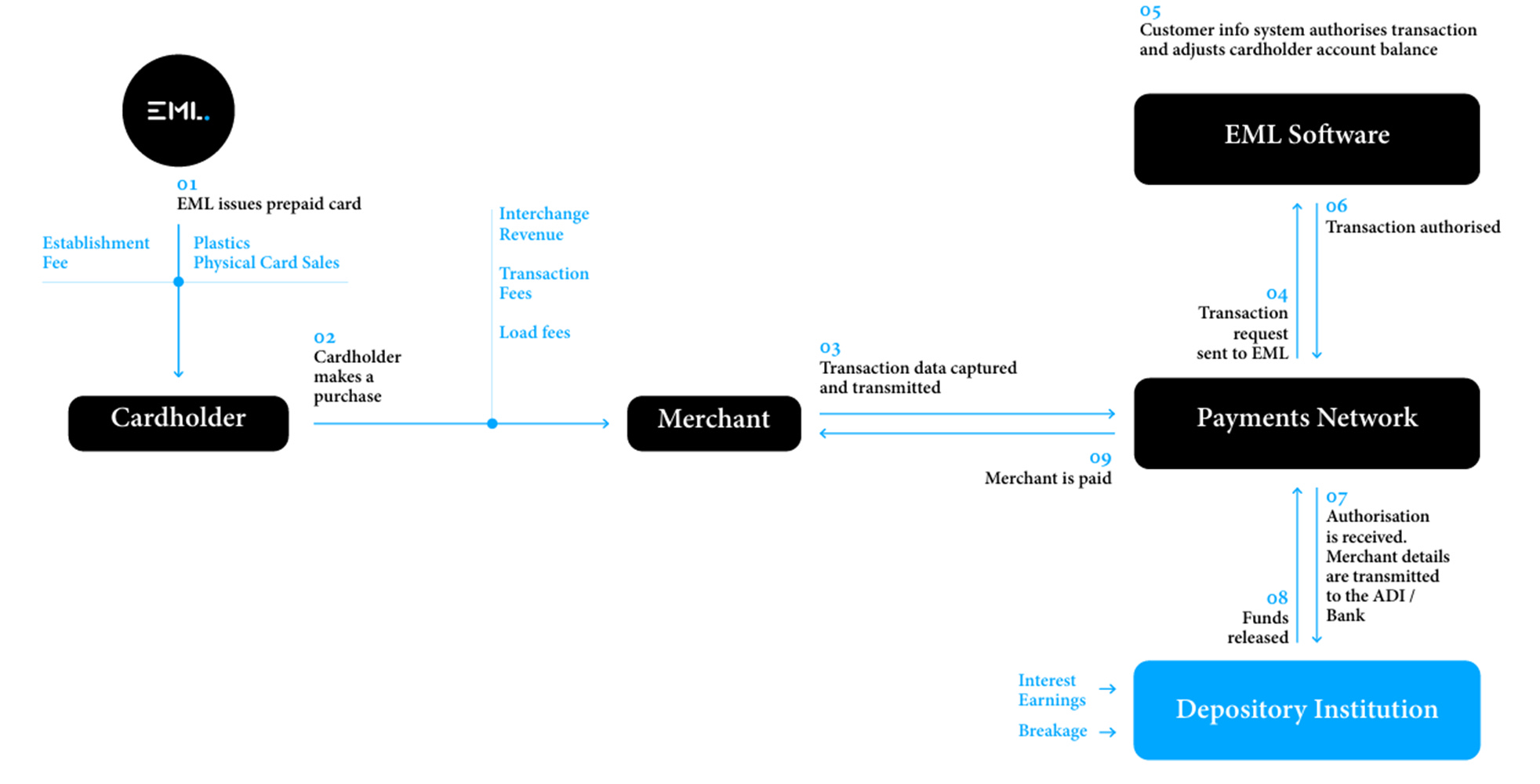

Let's start with how the Company actually makes money - EML's core business model and some of the key fees it earns are depicted below:

As you can see, the Company levies fees at various points in the prepaid payments process. Fee structures (flat vs. percentage, take-rate, etc.) vary greatly based on the type of transaction, customer size, etc.

These fees are either earned entirely or split with a banking sponsor when partnering with issuing banks (namely in the U.S., where the Company is unable to self-issue its prepaid cards due to regulation). Major COGS drivers include plastic costs for cards, bank sponsor fees incurred by EML when partnering with sponsor banks, and network fees paid to payment networks like Visa and Mastercard.

You can think of the Company's fees as broadly falling within the following four categories - 'Recurring' in this context simply refers to fees derived from payments-related volume on EML's cards. Note that the below percentages are PF based on my own estimates:

Recurring Revenue - Transaction (~52% of PF FY24 revenue): Fees incurred when a customer uses the card, including interchange (fee paid by the merchant's bank to the card issuer when a customer spends using the payment network, passed through to the customers), transaction fees (per transaction fees for prepaid cards, often levied when used abroad), and load fees (levied when reloadable cards are funded)

Recurring Revenue - Service (~18% of PF FY24 revenue): Further broken down into breakage, account management fees ("AMF"), and other. Note that breakage and AMF revenue can be recognized ahead of cashflow receipt (accrued as contract assets) - Happy to discuss the accounting in more detail in the comments in case of interest

Breakage Revenue (~8% of PF FY24 revenue): Unused amounts (i.e. residual non-refundable, unredeemed, unspent funds) from non-reloadable products after expiry that the Company is entitled to. This is 100% margin for the Company

AMF Revenue (~7% of PF FY24 revenue): Monthly charges on cardholder accounts, including dormant account fees charged after a certain period of card inactivity (typically charged monthly until the card is used or until there are no funds remaining)

Other (~3% of PF FY24 revenue)

Non-Recurring Revenue - Service (~6% of PF FY24 revenue): Largely establishment fees, reflecting fixed upfront fees for setting up a card program and the resale of plastic cards

Interest Revenue (~25% of PF FY24 revenue): Interest generated on float (i.e. value loaded onto the card held as cash by EML or its banking partners). This is again a 100% margin revenue stream and therefore highly valuable

EML will naturally be impacted by declining rates, although it's difficult to precisely calculate - It's hard to know where rates will ultimately settle and one would expect some offset in the form of looser monetary conditions driving transaction volumes over time. Still, it's worth noting that ~40% of the Company's interest revenue is generated by bonds that have staggered maturities over the next 4yrs (weighted average bonds maturity of 1.9yrs), offering some near-term hedging

Going a level deeper, the Company breaks out the following three segments. We'll focus on the two core segments, which should help provide a better sense of the Company's solution exposures and underlying growth rates. Again, the below percentages and margins are PF based on my own estimates:

Gift and Incentive ("G&I"; ~40% of PF FY24 revenue, ~79% gross margins): Provides single-load gift cards to over 1,000 gift and incentive programs including consumer gift cards available at malls, corporate-funded incentive cards for consumer promotions, and corporate-funded employee rewards cards

General Purpose Reloadable ("GPR"; ~55% of PF FY24 revenue, ~73% gross margins): Offer businesses and governments cards that can be reloaded multiple times with cash and have no set expiry date. Designed for consumer disbursements, employee benefits and rewards, digital wallets, and gaming

Digital Payments ("DP"; ~5% of PF FY24 revenue, ~76% gross margins)

G&I (~40% of PF FY24 revenue, ~79% gross margins)

The G&I segment processes ~AU$1.75bn in GDV, with ~67% from Europe (including the UK), ~22% from North America, and ~11% from Australia (a directional proxy for revenue split, but revenue/GDV yield can vary). ~88% of the segment's revenue is derived from customers (i.e. transaction and services revenue), with ~12% derived from interest. These underlying revenue streams grew ~3% and ~108% YoY, respectively, in FY24, driving segment revenue growth of ~9% YoY.

G&I's largest vertical is shopping mall gift card programs (sold both online and in-store), which I directionally estimate to be ~75% of GDV (based on FY19 numbers), with customers such as Unibail-Rodamco-Westfield (UK and Europe) and Simon Malls (US).

My understanding is that, depending on the program, these gift cards can be either open-loop (linked to one of the main payment networks like Mastercard or Visa and used anywhere where that payment network is accepted) or closed-loop (restricted in some manner to the specific mall or select retailers).

Mall gift cards are a popular holiday purchase and therefore a highly seasonal product - Equity research firm Edison estimates that this part of the business generates ~50% of its GDV in the 8 weeks before Christmas and a large proportion of breakage in the subsequent months.

Pre-COVID, this part of the business generated revenue/GDV yields of 700-800bps, driven in part by large structural breakage. While historically strong, EML's mall volumes have struggled post-COVID as a result of slower customer spending (given macro headwinds) and customer attrition as the Company dedicated resources elsewhere (acquisitions, aforementioned regulatory issues, etc.).

The Company saw mall revenues decline by ~5% YoY in FY24, in part driven by the run-off of a key customer - While hard to handicap, the Company is refocusing and revamping this business' go-to-market strategy to return to growth.

The remaining portion of the G&I segment is largely made up of corporate incentives. These are programs that allow companies to offer pre-loaded incentive or rewards cards to employees or customers, including cash back on purchases of high-value items (an example cited by Edison is Fujitsu A/C offering an AU$400 prepaid Mastercard gift card at purchase) or bonus schemes for employees.

Yields are typically lower in this segment at ~400bps, driven by structurally lower breakage (as these cards are more typically open-loop). This business has continued to show strength, growing ~16% YoY in FY24.

GPR (~55% of PF FY24 revenue, ~73% gross margins)

The GPR segment processes ~AU$7.8bn in GDV, with ~55% from Europe, ~7% from North America, and ~38% from Australia. ~65% of the segment's revenue is derived from customers, with ~35% derived from interest (driving ~80% of total interest revenue for the Company). These underlying revenue streams grew ~7% and ~99% YoY, respectively, in FY24, driving segment revenue growth of ~27% YoY.

GPR is a generally more diversified segment, and it's therefore more complicated to derive specific exposures, but we know key verticals include government and human capital.

The government vertical helps support local authorities, governments, and NGOs/charities make payments, pay benefits, and offer grants to beneficiaries and citizens. This vertical exhibited strong ~15% growth YoY. Importantly, this is despite PFSL (which has exposure to this vertical) having regulatory caps on growth for most of the year (through April 2024). We could see this vertical growing even more strongly with a full year of uncapped growth opportunities.

The human capital vertical is largely related to the Company's salary packaging offering in Australia, where EML is the main supplier in the space with dominant market share (working with all major Australian salary packaging services companies). This is a pretty incredible achievement - The Company started this business organically in 2017 and now has >90% of the market.

Briefly, salary packaging is an Australian tax incentive that allows employees in certain industries to increase their disposable income by paying for certain expenses in authorized expenditure categories from their pre-tax income. EML works with salary packaging services companies to provide prepaid cards focused on the Meals and Entertainment and Living Expenses expenditures categories, with a particular focus on public and healthcare industry workers.

The Company earns monthly fees per account plus interchange every time an account holder spends from their cards. This is an important, high-quality, resilient revenue stream for the Company, and also continues to grow strongly, with 23% growth YoY.

Thanks for the write-up. Think the company should be valued at 8x EBITDA really. Don't think they deserve the broken business valuation right now. Decent re-rate today at least

interesting article and stock.

But what is the reason for recent crash of share price? Change in management or/and results?

If it is the former, what happened that there was a 22% slump?