On Histogen ($HSTO) and Estimating Liquidation Proceeds

Histogen ($HSTO", or "the Company") is a broken biotech. Following an announcement of strategic alternatives in July 2023 and pausing development of its main drug, emricasan (focused on immune function), Histogen announced board approval of a complete liquidation and dissolution of the Company (i.e. distributing the proceeds from the sale of any net assets to shareholders).

I'll start by saying this isn't a liquidation I'm buying, but rather one I'm using to help better judge biotech liquidations in the future (these seem to have become more common in the current macro environment). Shareholder approval is ultimately still required to go through with the liquidation (shareholder meeting expected in Q4 FY23E). Given no proxy has been filed to date, there's not yet any management estimate of potential distribution proceeds to shareholders.

I look at most announced biotech liquidations, typically waiting until management's distribution estimates are released before making any purchases, however there's likely opportunity if one can reasonably estimate what liquidation proceeds will be prior to management estimates being disseminated to the market. Moreover, it's a good spot check on proxy assumptions.

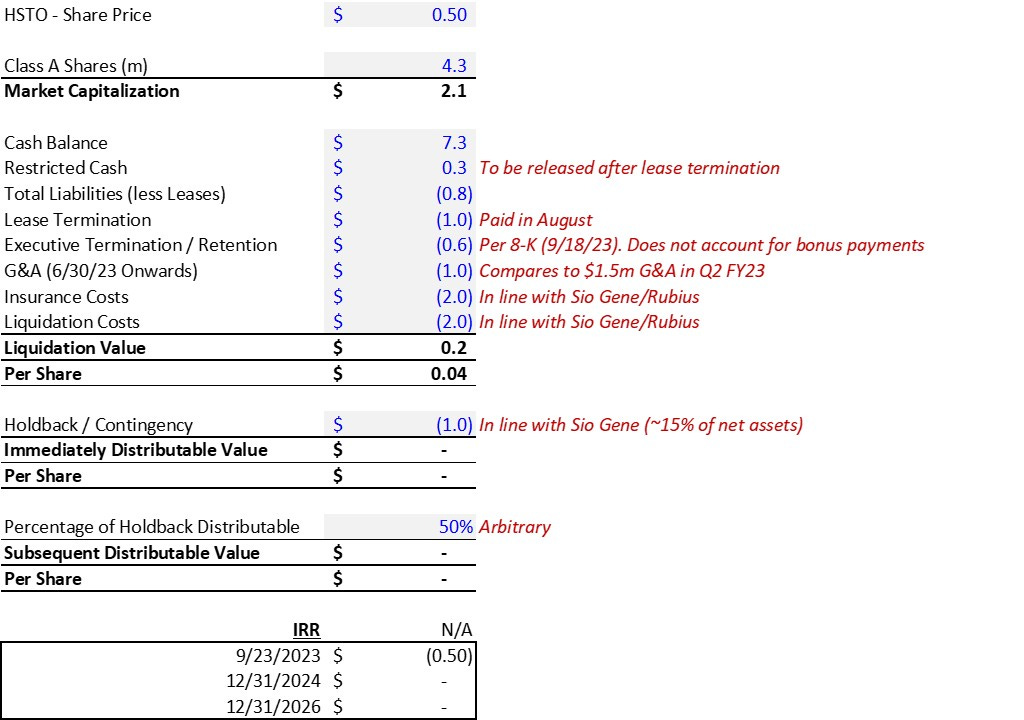

Histogen is a good example to use as it seems like a fairly straightforward liquidation. The Company has ~4.272m shares outstanding, with a lot of share turnover in the last few days in the $0.50 range, indicating a market cap of ~$2m. Per the Q2 FY23 (6/30/23) balance sheet, the Company had ~$7.3m in cash, no A/R, and total liabilities of ~$5.3m, indicating net current asset value ("NCAV") of ~$2m, right in line with the current market cap. However, ~$4.2m of the liability base is made up of operating leases associated with the Company's HQ and laboratory. Digging into the footnotes, we can see these leases have already been broken, with the Company paying a termination fee of $1m, offset by the release of ~$0.3m in restricted cash, fully eliminating the ROU assets and operating lease liabilities.

Per the 10-Q:

"On August 7, 2023, the Company entered into a Lease Termination Agreement (the “Lease Termination Agreement”) for its headquarters and laboratory operating lease […] subject to a termination fee paid by the Company of approximately $1.0 million. […] The lease termination will eliminate the Company’s right-of-use assets and operating lease liabilities […] [and] reclass $0.3 million of restricted cash to cash and cash equivalents."

Adding the ~$0.3m in restricted cash to the cash balance gets me to ~$7.6m in total cash vs. ~$1.8m in total liabilities (~$5.3m in total liabilities less ~$4.5m in operating lease liabilities plus $1m in lease termination fees). This gets me to an updated NCAV of $5.8m. Per the most recent 8-K released on 9/18/23, the Company expects to pay an additional ~$0.6m in termination/retention fees for outgoing executives and the new CEO (previously the COO/CFO, now in all three roles). These calculations exclude potential bonus payments if a certain amount of assets are sold within 90 days.

Following the July 2023 strategic alternatives announcement, the Company paused product development activities to reduce operating costs. I expect this to mean that all R&D expenses will fall away (~$0.5m in Q2 FY23) and that G&A (~$1.5m in Q2 FY23) will decline materially on a go-forward basis. Keep in mind that rent and salaries will still largely be paid through Q3 FY23E, however termination of the lease and the majority of the employees (only 2/6 total Q2 FY23 employees will stay with the Company to help with the liquidation) will be reflected thereafter. Let's arbitrarily assume ~$1m in G&A from 6/30/23 onwards.

The only remaining costs to think through are insurance costs (believe largely in relation to directors’ and officers’ liability insurance), ongoing liquidation costs (lawyers, bankers, accountants, wind-down administration services, etc.), and a contingency reserve / holdback (to satisfy contingent, unanticipated liabilities as they become due). In terms of insurance and liquidation costs, I looked at proxies from recent biotech liquidations including Sio Gene and Rubius Therapeutics (I'm a shareholder in the latter). Costs for companies of this size tend to be in the ~$2m range for each of insurance and liquidation costs, so let's assume that for now. The holdback is more difficult to estimate and subjective - Sio Gene held back ~15% of net assets (total cash less total liabilities), so using that assumption would get us to ~$1m in the reserve.

Putting it all together, I get to negative liquidation value, implying shareholders won't get anything out of the process (my math is below). Given the stock trades at $0.50, the market definitely doesn't agree with me. It's definitely possible I'm missing something - My G&A, insurance costs, liquidation costs, and holdback assumptions could be too aggressive. Out of conservatism, I'm also not ascribing any value to the Company's PP&E (>$1m gross) or the Company's pipeline assets, but I'm really not smart enough to determine/handicap if those will be worth anything.

This is one I'll be monitoring to see where the ultimate distributions end up and how far off I am vs. the market.